It is often said that history doesn’t repeat itself but it often rhymes. The term ‘Groundhog Day’ refers to a situation in which a series of unwanted events appear to be recurring in a similar way.

The world though extremely complex can be simplified to an extent via observing and learning from similar past historical events. The inability to predict the probability of key historical events has been a fallacy for humans (let alone investors) for ages, be it predicting natural disasters, outburst of diseases or recessions. While predicting such events is difficult, understanding the outcomes and reaction to the same serves as an important guide.

This edition of our Investor Compass focuses on the recent RBI decision to withdraw Rs.2,000 notes from circulation. We take a look at the likely consequences from this action while drawing parallels from the 2016 de-monetization event and most importantly how it might affect our portfolio companies.

The event – Withdrawal and not de-monetization (yet)

- RBI on 19th May, 2023 announced the withdrawal of Rs. 2,000 notes from circulation, adding that the notes will continue to be legal tender. The existing Rs 2,000 notes can be deposited or exchanged in banks until September 30, 2023, with a limit of Rs 20,000 at a time for exchange.

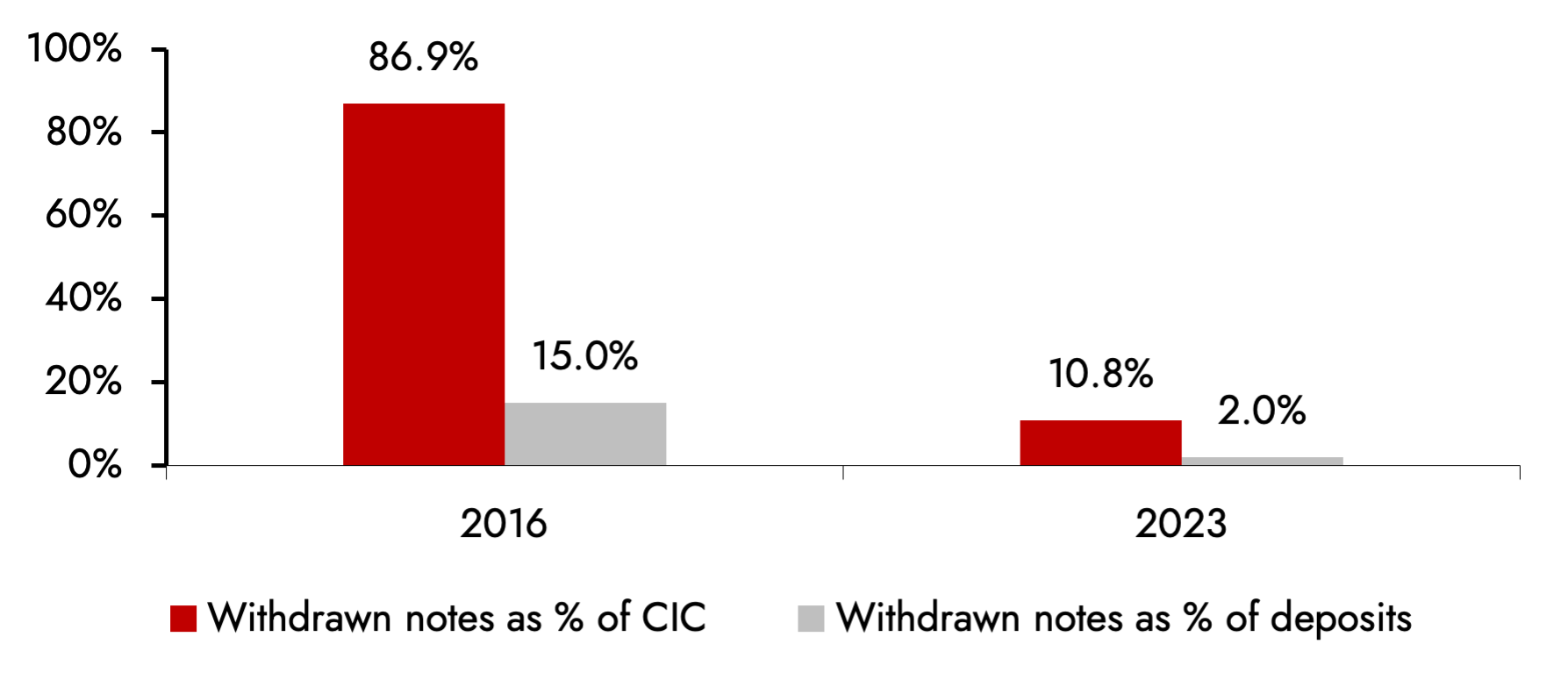

- This event, which is being compared to the 2016 Demonetization, defers materially as Rs. 2000 notes continues to be legal tender. In addition to the same, the intensity of the impact is expected to be limited (if any) since these notes constitute 10.8% of Currency in Circulation and 2% of deposits, unlike 86.9% / 15% during 2016 (Refer Exhibit 1). Moreover, the time-frame for this withdrawal is 4 months compared to immediate impact during de-monitization

Exhibit 1: Impact of withdrawal of Rs2,000 notes is expected to be limited given the lower share

Source: Ambit Asset Management, RBI

In an ideal world, the above event should be a non-event provided everyone in India acts rationally as there is no change in acceptance or usage of Rs.2,000 note. However, going by historical precedence along with our assessment of on-ground trends we anticipate some impact (if any) on Banking and pockets of Consumer Discretionary sectors

A. A positive Impact on Banking sector due to:

- Increase in Liquidity – Increase in near term banking liquidity due to anticipated currency deposits of ~Rs3tn by Sept’23. Withdrawal of liquidity, however, will be phased out over next 3-4 quarters.

- Growth and business activity – Total Rs2,000 notes in circulation is ~Rs3.6tn constituting ~2% of overall system deposits. While there is a restriction of Rs20,000 on the exchange of these notes, there is no restriction on deposit for the same. We anticipate it as a marginal positive for deposit growth of banks in term near-term. It is important to note that deposit growth for banks has been lagging loan growth thus far.

- Impact on NIM’s – Deposits with banks is likely to increase in near term to the tune of ~Rs1.5-2tn (net of exchange) which will lead to fall in higher cost Certificates of Deposits (CD) issuances and likely easing of deposit rates, thereby impacting NIMs positively.

- Impact on G-Sec Yield – The increase in deposits is likely to ease G-Sec yields as banks look to park these deposits in Government bonds

B. Consumer Discretionary, Retail and even Real Estate may see some panic spending:

In addition to the short term impetus on banks, based on current ground level checks the number of enquiries for gold, high-end discretionary products and pockets of real estate have increased sharply post the announcement by RBI. Consumers may advance future high-ticket purchases in order to utilize the withdrawn notes.

Conclusion:

We do not anticipate any major adverse impact on any of our portfolio companies because of the above event.

On the contrary, we anticipate the banking sector to be a beneficiary of the above. While the current event cannot be compared to the 2016 demonetization, we see a likelihood of repeat of the human behaviour (though on a smaller scale) which may aid short term demand of several discretionary and building material companies in the portfolio. Overall we envisage the above event to be neutral to slightly positive to our portfolio companies.

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - aiapms@ambit.co | Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020